Toronto Star: ‘Paycheque to paycheque.’ Inflation is hitting low-income Canadians hard — and its effects are likely to be long-lasting

Posted August 8, 2022

Posted August 8, 2022

:format(webp)/https://www.thestar.com/content/dam/thestar/business/2022/08/06/paycheque-to-paycheque-inflation-is-hitting-low-income-canadians-hard/consumerspending_web.jpg) At first, the headlines about inflation Jordann Brown was reading in the spring of 2022 didn’t seem to be bearing out in real life.

At first, the headlines about inflation Jordann Brown was reading in the spring of 2022 didn’t seem to be bearing out in real life.

The Halifax-based content marketing manager said she carried on working from home, shopping for groceries, and saving for the future.

Then, one day a couple of months ago, she went to fill up her car and realized it now cost her $95 to fill up her tank, when a year earlier it had cost $65.

“That was a really, really noticeable difference,” she said. “And I was like, ‘OK, this is going to be a problem.’”

Now, everything in Brown’s life is more expensive, such as visiting her family three hours away — her parents are coming to her more to help shoulder the cost. Brown has been organizing more backyard evenings with her friends instead of going out. She’s doing more online comparison before she shops for groceries, and is hitting Costco more frequently to buy essentials in bulk. When she enters the grocery store, if she sees a staple food like chickpeas on sale, she grabs extra.

It’s an experience that likely sounds familiar: the extra caution when you buy your weekly groceries, the sharper eye for sales and promotions, the additional flexibility in your meal plan when you find a good deal. Most Canadians are adjusting to inflation not only at the grocery store, but in other ways. They’re driving less often to save on gas, pushing back or cancelling home renovations, having a staycation instead of flying abroad.

But for low-income Canadians, there’s a lot less to trim. Inflation is making it difficult for millions to afford the basic necessities, including food and housing. Many must make difficult decisions that could land them in high-interest debt, deplete any savings they might have, and even see them go hungry.

Inflation is hitting low-income people in a much different way than it is many of us, highlighting the fault lines of society that the COVID-19 pandemic had already deepened. And even if we get inflation under control, its effects will be long-lasting for the most vulnerable among us.

Living paycheque to paycheque

Shelly Ann Allan has been looking for a new place to live amid record inflation and rising rent prices, after her landlord evicted her. In the meantime, it’s not just rent that’s become more expensive, but everyday expenses like food — she avoids the grocery store unless she absolutely has to go.

“I’m living paycheque to paycheque,” said Allan, who works full-time as a material handler and is also a member of advocacy group ACORN.

Normally, Allan sends money home to her family in Trinidad, but for the past several months she’s been unable to send much, if at all. She’s thought about getting a second job, but doesn’t have the energy to work in the evening after a nine-hour day.

“No matter how hard I work … it’s not working,” she said.

Allan is one of millions of Canadians for whom inflation isn’t just a nuisance — it’s forcing them to cut down on things they need to survive. Throughout the pandemic, women, low-income, racialized, and otherwise vulnerable people in Canada were most affected by unemployment and pandemic restrictions, and they’re now emerging into a world where life costs more by the day.

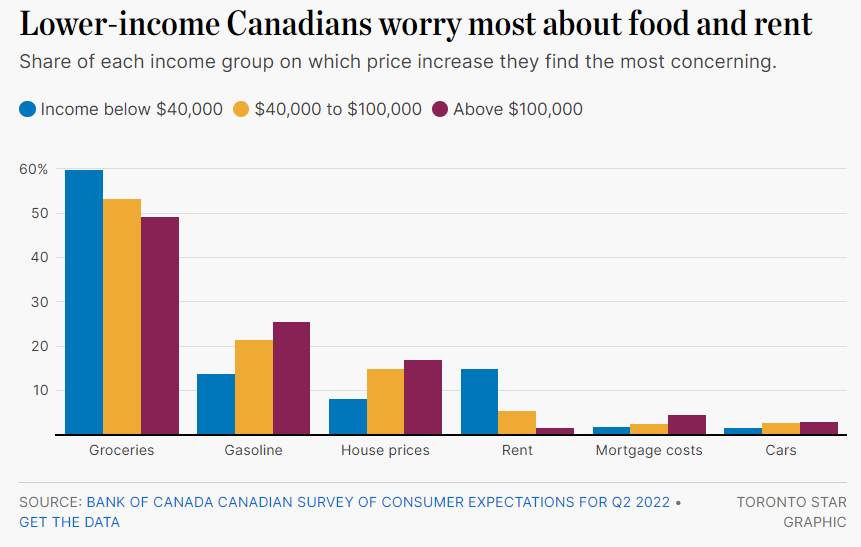

According to the Bank of Canada, while the cost of food tops everyone’s list of inflation stresses, low-income Canadians are more worried about affording food and rent than people who are middle- or high-income.

Lower-income people spend everything they get already, said Canadian Centre for Policy Alternatives senior economist David Macdonald, and inflation will make it harder and harder for those workers to meet their basic needs.

It’s not surprising that food is one area where Canadians are feeling the biggest pinch — it’s a necessity, after all, and also a key driver of the current inflation rate. Butter was up more than 20 per cent in June year over year; whole chicken almost 16 per cent, white bread 14.5 per cent, pasta almost 21 per cent.

That’s why so many of us are keeping an eye out for sales and promotions, as well as choosing cheaper alternatives like private labels wherever possible, according to recent consumer surveys.

Shoppers tend to substitute with cheaper products in the face of high costs, said Macdonald. For families with room to trim their food budget, this might help stave off the effect of inflation. But those who are already operating on a tight budget, like Allan, will feel the pinch right away.

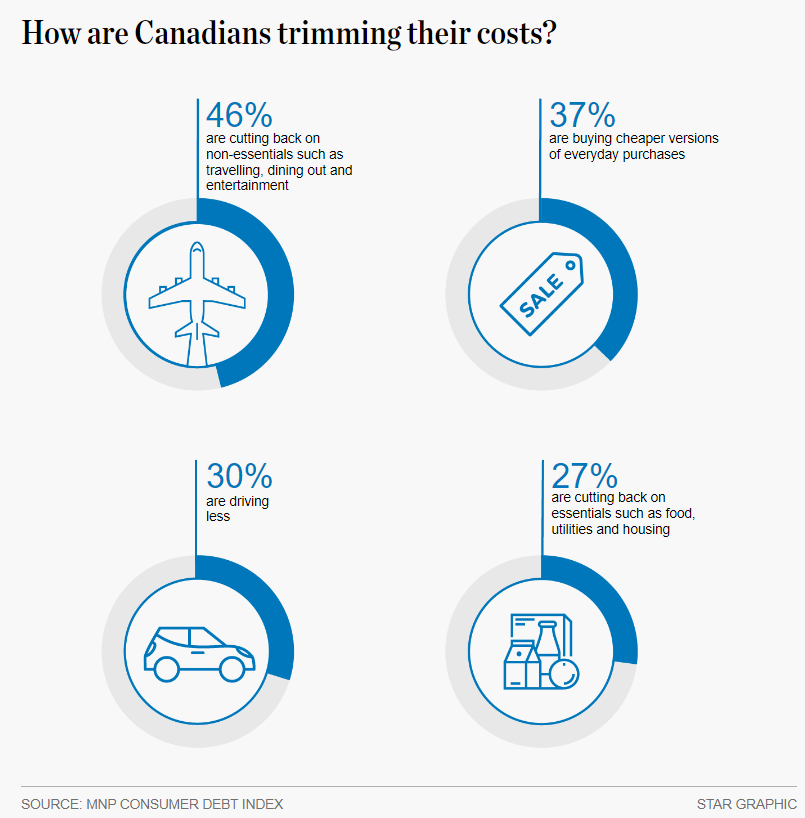

More than a quarter of Canadians are being forced to cut back on essentials such as food or utilities to make ends meet, according to an Ipsos survey on behalf of insolvency firm MNP in June. Women and those aged 35-54 were more likely to say they were cutting back on both essential and non-essential items and services.

Meanwhile, many people will turn to their savings or forms of debt to get by, said Macdonald, noting that credit card balances have begun to rise from their pandemic lows.

Lower-income workers, younger adults, people with disabilities, households with children, and racialized groups are all more likely to be borrowing extra money to stay afloat, Statistics Canada found.

And while the Bank of Canada is raising interest rates at an unprecedented clip, it doesn’t have power over gas prices or food, and so for many Canadians, nothing is getting cheaper.

This may drive more people to use services like food banks in the coming months, the Statistics Canada survey found, especially those with children at home.

Post-pandemic spending sprees dampened by inflation

But while some households are trying to string together enough to make it through the month, others have plenty of room to trim. Despite the inequalities deepened by COVID-19, Canadians emerged from the pandemic with a collective $300 billion in excess savings, and many were ready to spend on what they missed the most — food, travel, and entertainment.

Surveys show consumers this spring were eager to travel, eat at restaurants, and enjoy their cities again, even if it meant spending a little extra — many said they planned to spend significantly more in the coming year.

As 2022 wore on, pre-pandemic spending trends began to re-establish themselves, said TD economist Ksenia Bushmeneva, with consumers spending more on things like entertainment, recreation, and restaurants. Travel spending went up too, despite delays at major airports in Canada and worldwide, according to the Conference Board of Canada.

But as everything gets more expensive, while the dollar amount spent might go up, the quantity of purchases may decline, according to the Bank of Canada — Canadians might have some extra cash, but they’ll get less for it.

And they’re noticing. As the summer approached, Canadians started to get a little more frugal.

Canadians are feeling less and less optimistic about their finances due to inflation, and are adjusting their spending habits accordingly, resulting in a slowdown of consumer spending growth in June, according to the Conference Board of Canada.

As the average transaction size at the gas pump climbed significantly in 2022, Canadians weren’t buying gas much more frequently than they were a year ago, even though restrictions have eased and people are going back to the office.

That may be linked to a significant increase in travel by bus and train, according to Moneris — both for daily commutes and longer journeys. As well, some workers may be choosing to continue working remotely in part because of the high price of gas.

And retail sales data shows that while spending may be up in dollar amounts, “real” sales, or the amount of stuff people are getting for their dollars, are not as elevated, said Bushmeneva. In other words, a significant portion of that rise in spending is due to prices getting higher, not people making more purchases.

For example, retail sales were up 2.2 per cent in May, but in volume terms were up only 0.4 per cent.

An advance estimate of retail sales from Statistics Canada shows that in June, retail sales in dollar amounts increased only 0.3 per cent, which Bushmeneva predicts means in terms of “stuff,” people are buying less than they did in May.

“In real terms, retail sales have probably fallen,” she said.

The MNP survey found that almost half of Canadians were cutting back on non-essentials like travelling, dining out or entertainment, and many were looking to save by cutting down on gas and seeking out cheaper versions of everyday purchases. And yet in June, Canadians were still spending more per transaction at bars, restaurants and fast food places than they did pre-pandemic, according to Moneris — likely due to inflation.

Canadians are also spending less on their homes. Foot traffic data analyzed by Avison Young shows that people are frequenting big box stores less as the year progresses — likely due to a drop in visits to the hardware store, said Marie-France Benoit, director of insights for AY in Canada.

For one, the renovation boom is subsiding as people venture out of the house and as interest rates rise, she said. As well, hardware stores are likely taking a hit because inflation-wary consumers are postponing large purchases such as home renovations.

Financial wellness educator Zandile Chiwanza said when inflation hit her she had to take a step back and reconsider her approach to spending. With pandemic restrictions lifting, she wanted to spend on things that would bring her joy, but worried about her long-term savings goals.

For example, Chiwanza wants to visit her family, but the price of a ticket has tripled.

She’s doing everything within her control to save, such as spending loyalty points and taking advantage of sales.

“I am using all of my tools in the tool box right now,” she said, but “I’m still spending more.”

Brown, too, is budgeting carefully when it comes to non-essentials like travel, a new car, or clothing. She feels fortunate to have locked in a fixed rate on her mortgage last year, but knows she has to prepare for renegotiation and higher rates when the term is over.

But like Chiwanza, Brown knows it could be much worse. She is significantly better off than she was when she was younger, and she knows that if things get worse, she can take her budgeting to the extreme.

“I’ve lived on a lot less than I have now. So if push comes to shove, I can reduce my spending pretty dramatically.”

Inflation fades, prices remain

The Bank of Canada’s answer to inflation has been to raise its key interest rate in an effort to cool the housing market and create a better balance for Canadian households. But in the short term, that means just another cost for consumers. Those rising rates are starting to affect almost two-thirds of those surveyed for MNP, and half of respondents said if rates kept rising they would be in financial trouble.

MNP president Grant Bazian thinks insolvencies and bankruptcies will go up in 2022 as a result of rising unaffordability.

“Prices definitely don’t seem to be going down,” said Bazian.

“(People are) having a really hard time making ends meet.”

Consumers can take heart in the fact that there are signs inflation is subsiding — but they should also remember what that actually means. Inflation is, by definition, an increase in prices. So if inflation slows down to a more normal pace, that doesn’t mean prices will go down across the board — they’ll just rise at a slower rate.

Meanwhile, wages have not been keeping up, and many income assistance programs are not indexed to inflation, noted Macdonald. Many households struggled to pay for the essentials before the pandemic, he said, and though COVID-19 assistance programs buoyed some for a while, many people will be right back where they started pre-pandemic, if not worse off.

In other words, inflation may subside, but for the most vulnerable among us, the damage is already done.

***

Article by Rosa Saba for the Toronto Star