Lowering the interest rate of predatory installment loans is the right thing to do!

Posted January 25, 2024

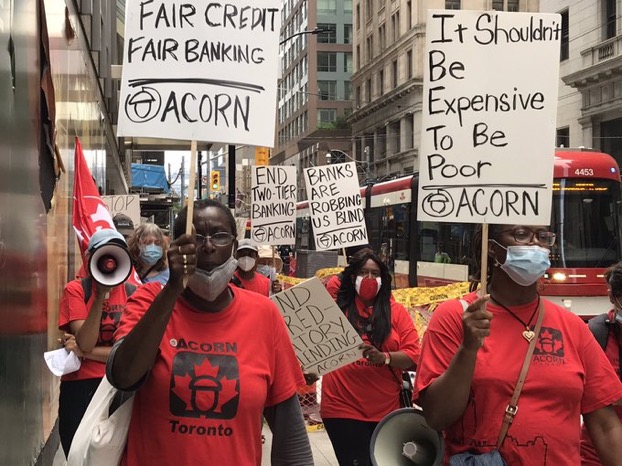

ACORN Canada, a national community union of low-and- moderate-income people, has fought long and hard to push the federal government to lower the criminal interest rate. Currently, fringe lenders such as Money Mart, Easy Financial, Cash Money and many others are legally allowed to charge an annualized percentage rate (APR) of 48%. On top of this, lenders can charge insurance, fees etc. This is extremely exorbitant and forces people into a debt trap.

The Canadian Lenders Association (CLA) is alleging that lowering the interest rate of instalment loans will throw these lenders out of business and people will not have access to credit. This is misinformation. CLA is sending out threatening letters to borrowers to this effect.

Read a joint statement by ACORN and Momentum.

It is deeply concerning that some of the big banks such as BMO, RBC and TD are also members of CLA and therefore are taking part in this letter writing campaign.

Tell the banks to support lowering of the interest rate of predatory instalment loans.

ACORN continues to fight for further lowering of the interest rate and fair credit alternatives.

ACORN’s periodic surveys show the devastating impacts of these loans on the most vulnerable people.

Some of the key findings from ACORN’s latest survey conducted in 2023 include the following:

- ⅓rd of the respondents said that their loans got refinanced multiple times – a common tactic that predatory lenders use to ensure people are in the debt trap forever.

- Impacts people reported as a result of being in high interest debt included not being able to buy basic necessities (66%), followed by inability to pay a different bill (48%), reduced amount of savings for retirement (40%), skipping a needed medical appointment (29%) and incurring overdraft fees (26%).

- Consequences of NOT making all or most of the high interest loan payments reported by borrowers:

- 80% of respondents reported stress, anxiety and depression.

- 72% reported it caused them to get into even more debt.

- 67% reported adverse effects on their credit score.

- The majority of respondents were highly unsatisfied with the high-cost loan.