Jacobin: Despite Record Profits for Canada’s Big Banks, Customer Fees Keep Going Up

Posted December 15, 2021

Posted December 15, 2021

Christmas is coming early for Canada’s bankers.

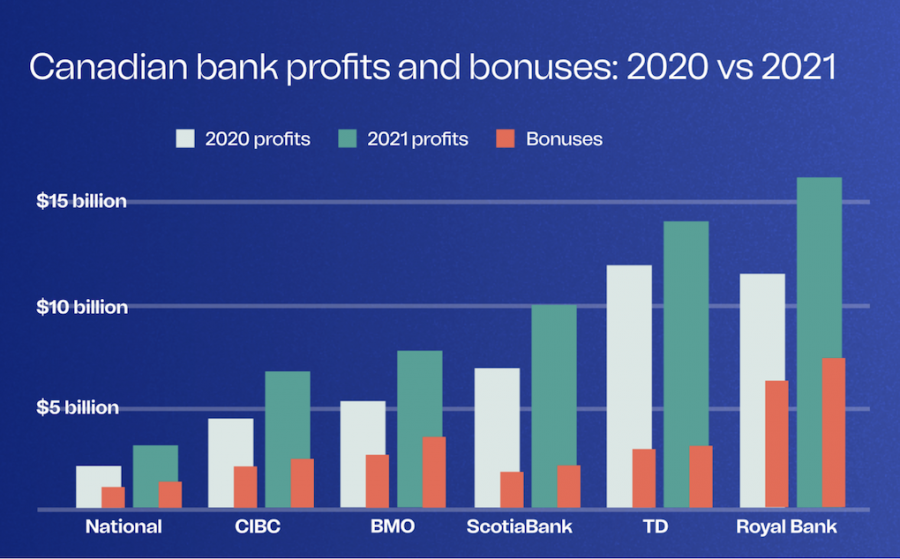

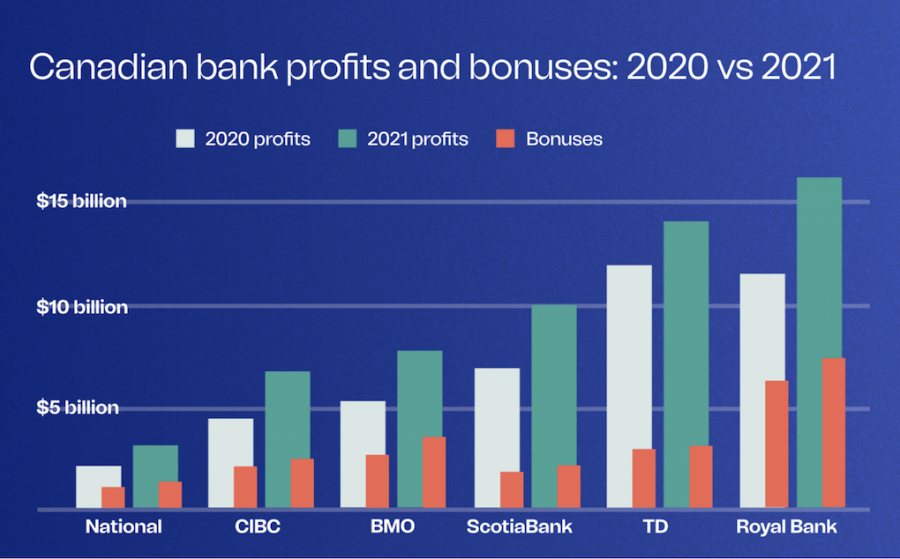

The six largest banks hit record-breaking profits in 2021 and will pay out massive bonuses at the year’s end, newly released fourth quarter earnings reports show. On the strength of a combined $57.4 billion in profits, the Big Six are paying out $18.8 billion in bonuses before the holidays.

This year’s bonuses follow on the $15.2 billion paid out by the banks in 2018, $15.6 billion in 2019, and $16.2 billion in 2020, making this the best year in history for high-level bankers in Canada. Canadian banks are among the most profitable companies in the world, and the North American nation has become an increasingly favorable place for banks to operate.

Despite their runaway profits, banks offered only temporary and limited support to customers during the pandemic. Not only have most of those supports expired, but banks are raising fees again. As pandemic-related federal income supports like the Canada Recovery Benefit (CRB) are phased out, nearly half of Canadians are $200 or less away from covering their financial expenses each month.

According to a survey in October, more than a quarter of Canadians are already insolvent, having no money left by the end of the month to cover their bills.

According to a survey in October, more than a quarter of Canadians are already insolvent, having no money left by the end of the month to cover their bills.

This quarter solidified the Big Six banks’ major rebound this year. Scotiabank netted $9.95B, the Bank of Montreal (BMO) $7.7B, the Royal Bank of Canada (RBC) $16.1B, the Toronto Dominion Bank (TD Bank) $14.2B, the National Bank of Canada (NBC) $3.1B, and the Canadian Imperial Bank of Commerce (CIBC) $6.4B.

Business as Usual for Canada’s Banks

While bank earnings have almost always been steady, they’ve ballooned over the last decade thanks to wealth management divisions and mortgage provisioning amidst a red-hot housing crisis. Mergers and acquisitions, credit lending, and providing daily banking services to customers provides banks with a steady stream of income.

Canada’s banking sector has also long enjoyed optimal business conditions. A Toronto Star study found that banks in the country, from 2011 to 2016, paid the lowest tax rate — 16 percent — of all the G7 countries. Their penchant for outright tax avoidance helps as well, parking billions in offshore tax havens in Barbados, Antigua, Ireland, and beyond.

In times of crisis, they benefit from federal liquidity support or bailouts, often with few requirements. As the major banks received $115 billion following the 2008–9 financial crisis, their CEOs ranked among the hundred wealthiest in Canada. Last week’s earnings reports from the Big Six are only the latest development in the financial sector’s major rebound after brief pandemic dips.

In addition to a sooner-than-expected economic recovery, federal income supports helped avert insolvencies, with about a third of all Canada Emergency Response Benefit (CERB) payments going to people’s debt repayment. This infusion of public money, aided by a rebounding economy, meant the banks needed to access less of the money they’ve set aside to service bad loans in times of crisis (known as loan-loss reserves), boosting their bottom line.

By February 2021, the Big Six were more profitable than they were before the pandemic. Banks, in fact, have a new problem: they have more money than they know what to do with. Because the Big Six hold so much excess capital, shareholders expect the banks to maximize their investments, which can happen through increasing dividends or investments in their business.

Profits Flow In, Fees Go Up

Should we expect 2021’s huge profits to translate into more affordable services? Not likely. During the early months of the pandemic, the financial sector stepped in with a number of rare supports: cuts to interest rates for two to six months, for example, as well as a few months of mortgage payment deferrals. But a year and a half later, these interventions have mostly disappeared.

Last spring, just over a year after the COVID-19 pandemic hit Canada, the banks came under fire for raising fees on basic services. On TD Bank’s “preferred checking” accounts, for example, the bank raised its required minimum balance to waive fees from $2,000 to $5000, as CBC reported. Each transaction for customers who don’t have that minimum balance in their accounts will go up, too, by nearly two dollars. BMO, RBC, and CIBC brought in similar fee changes as well.

High fees are nothing new to Canadian banking. Compared to other countries, Canadians are charged steeply by banks to hold their money — some of the highest fees in the world. This includes fees for accounts and ATM withdrawals, as well as overdraft and non-sufficient fund charges, all of which burden those with the least amount of money.

Fees serve as an important — albeit comparatively small — source of profit during a period of continued low interest rates. Yet even after years of rock-bottom interest rates set by Canada’s central bank — meaning lending is cheaper than ever — most banks have maintained credit card rates at around 19.9 percent.

The Canadian Labour Congress and ACORN Canada have both led campaigns taking aim at how severely the deck is stacked against consumers. ACORN points out that about 3 percent of Canadians — almost 1 million — are “unbanked” and excluded entirely from basic financial services like checking accounts and credit. As the banks stave off demands to drop interest rates on credit cards, raise them on savings accounts, or slash fees, they’ve also laid off employees, closed branches, and reduced services.

Where Does All the Money Go?

So where has surplus from all these savings gone? Certainly, some is being invested in new technologies and other core business ventures. Giant amounts have also been allocated, year over year, to bonuses.

If past years are any indication, executives will receive enormous compensation this year. Typically, they earn millions in variable “performance pay” — which can include short-term incentives like cash bonuses, or long-term incentives like stock options — on top of their annual salaries, existing portfolios, pensions, and more.

In 2020, TD Bank CEO Bharat Masrani earned $8.9 million — consisting of a cash bonus, stock options, and deferred “performance share units” — in addition to his $1.45-million salary. David McKay, president and CEO of RBC, earned $10.8-million on top of his $1.5 million salary. BMO CEO Darryl White topped up his $1 million salary with $8.2 million in bonuses, including a $2.3 million cash bonus.

Other executives typically see eye-popping bonuses each year, and higher-ups in finance’s more lucrative areas — investment banking, for example — profit handsomely as well. In 2020, total compensation for BMO’s eleven senior executives — including salary and all other benefits — came out to $47.7 million. Total compensation for “other material risk takers” — senior staff that have the power to expose the bank to large financial risk — was $242.8 million.

Windfall profits also fund expensive and controversial stock buybacks, whereby a company buys back its own shares from investors. Like dividends, these give shareholders a big payout. The brief pandemic ban on stock buybacks and increases to dividend payouts expired at the beginning of November, meaning some of the huge amounts of capital in bank coffers — the billions in unused loan-loss reserves, for example — have begun padding the pockets of shareholders.

In addition to increasing dividends, all six banks announced stock buyback plans. Scotiabank is slated to repurchase up to 24 million shares; RBC up to 45 million shares; National Bank up to 7 million shares; CIBC up to 10 million shares; TD Bank up to 50 million shares; and BMO up to 22.5 million shares. Buybacks typically benefit a company’s executives as well. Buybacks boost share price, which is good for the upper crust given their compensation typically comes from stock options. But an increase in share price is also often a key criterion used to measure executive performance, which leads to even higher bonuses later.

Specifics on this year’s executive compensation will be found in each bank’s springtime “proxy circulars,” released ahead of banks’ annual shareholder meetings. All in all, decades of exorbitant profits have been funneled into assorted forms of bonuses and corporate ventures — high-level compensation, buybacks, mergers, and acquisitions — but not into making things more affordable for consumers. With such a small group of banks offering similar products at similar rates, the Big Six function more or less as an oligopoly, relatively immune to the normal pressures of capitalist competition.

***

Article by Dan Darrah for the Jacobin