CBC News: Budget 2021 sets up a fight over high-interest loans

Posted May 10, 2021

Posted May 10, 2021

Though it got only a few lines in the hundreds of pages that made up Budget 2021, the federal government’s commitment to open talks on changing Canada’s “criminal rate of interest” has anti-poverty activists bracing for a battle with high-interest lenders.

Though it got only a few lines in the hundreds of pages that made up Budget 2021, the federal government’s commitment to open talks on changing Canada’s “criminal rate of interest” has anti-poverty activists bracing for a battle with high-interest lenders.

It is currently a federal crime to charge interest over an annual rate of 60 per cent on any type of instalment loan or line of credit.

But Canada’s laws have left one kind of lending exempt from that prohibition. Short-term payday loans — usually due for repayment within two weeks — are regulated by the provinces and typically charge annualized rates of interest in the range of 400 per cent to 500 per cent.

While payday loans charge the highest interest rates, those who want the sector reformed are also alarmed by a newer trend: payday lenders offering longer-term loans or lines of credit.

Companies like Money Mart and Cash Money began to branch out into those kinds of loans after 2016, as provinces started to tighten the rules on what they could charge for payday loans.

Compared to bank rates, the interest charged on these loans is extremely high, often in the 45 per cent to 50 per cent range.

The ‘criminal’ interest rate

Those longer-term loans have to respect the 60 per cent annual interest limit — but critics like independent Sen. Pierrette Ringuette say that limit is still far too high.

“This 60 per cent criminal interest rate that was put in place over 40 years ago is no longer what is required in the Canadian marketplace,” she told CBC News as she prepared to table a bill that would fix the criminal rate of interest at 20 per cent over the Bank of Canada overnight rate.

“We’re at a time where the Bank of Canada rate is 0.5 per cent. So I honestly believe that 20 per cent over the Bank of Canada overnight rate is an adequate criminal interest rate for many years to come.

“This will be in place and can be in place for a very long time, and create stability that we need in this new modern era … We’re not in the 1980s anymore, [when] the Bank of Canada overnight rate was at 22 per cent, 23 per cent or even 24 per cent.”

But the industry’s lobby group says that “a reduction to such a rate would eliminate the sector and result in denial of access to credit from legal licensed lenders for millions of Canadians.”

The Canadian Consumer Financial Association (CCFA) — which represents Canada’s biggest payday lenders, operating about 900 retail outlets — said in a written statement that “with the reduction, it would not be financially viable to lend to a majority of borrowers who seek credit from our members.”

The loans industry said it plans to argue that the alternative to payday lenders is criminal loan sharks.

“If the government unintentionally eliminates access to credit, the need does not disappear and borrowers will turn elsewhere to unlicensed sources,” said the CCFA.

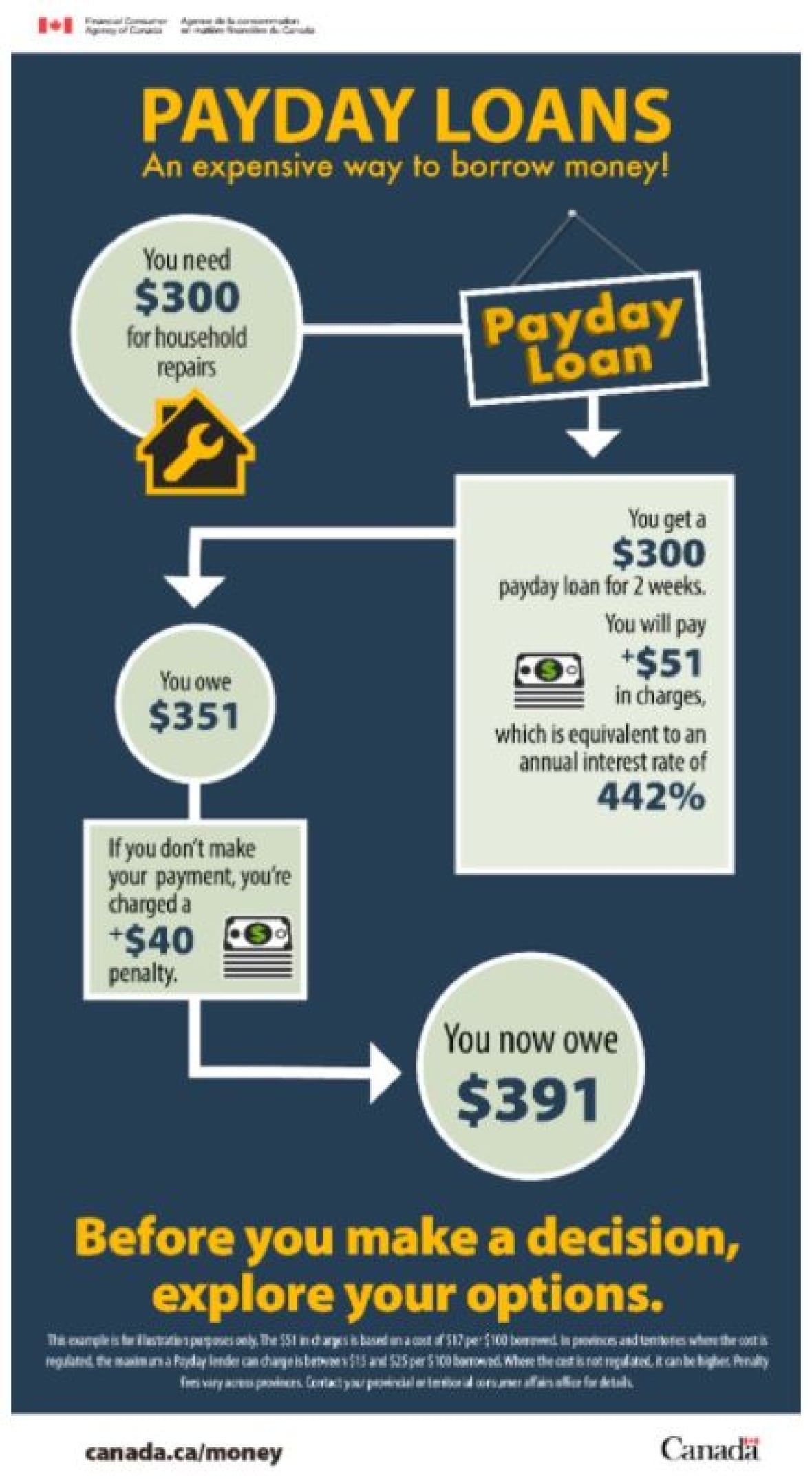

Canada’s Financial Consumer Agency has warned of the dangers of falling into a debt trap through high-interest borrowing. This agency infographic explains the different costs of four methods of borrowing $300 for 14 days. (Financial Consumer Agency)

The CCFA has been making that argument more and more in recent years as provinces and even cities have placed restrictions on their operations — and after the federal government launched a public information campaign to warn Canadians about the risks of using services which, according to the Financial Consumer Agency of Canada, “are very expensive compared to other ways of borrowing money.”

Bills take aim at industry

The industry has long been in the sights of anti-poverty groups such as ACORN, but is now increasingly being targeted by legislation.

New Democrat MP Peter Julian has campaigned for tighter regulation of the high-interest loan sector for years and currently has a private member’s bill on the topic.

“I’ll just give you one of many, many examples … A local constituent who borrowed $700 a few years back has paid $13,000 dollars in interest charges and still owes the $700,” he told CBC News.

“We’re talking about interest rates in real terms of 400, 500, up to 600 per cent annually. It’s legalized loan-sharking and at a time when Canadians are struggling, it simply should not be allowed.”

Julian said the rules that allow the system to charge those rates were “put in place deliberately” and he doubts the sincerity of the government’s recent commitment to consultations.

“The government’s attempt to pay lip service to it in the budget by saying, ‘Well, we’re going to consult on this’ is meaningless for all those Canadians who are struggling under these impossible debt burdens,” he said.

Like Ringuette’s bill, Julian’s C-247 proposes tying the criminal rate of interest to the Bank of Canada overnight rate, but with slightly more leeway for lenders — under Julian’s bill, they would be able to exceed that rate by 30 per cent.

Like Ringuette’s bill, Julian’s C-247 proposes tying the criminal rate of interest to the Bank of Canada overnight rate, but with slightly more leeway for lenders — under Julian’s bill, they would be able to exceed that rate by 30 per cent.

Katherine Cuplinskas of Finance Canada says the government is serious about fixing the problem.

“Over the past 15 months, we have put in place new, significant and expanded income support programs. These include the CERB, the Recovery Benefit and the expanded Employment Insurance (EI) program,” she said.

“Many lower and modest-income Canadians do, however, continue to rely on high-interest short-term loans to make ends meet, leaving them in a cycle of debt. That is why we are committing in the budget to fighting predatory lending. We will soon launch a consultation on lowering the criminal rate of interest in the Criminal Code of Canada on instalment loans offered by payday lenders.”

Cuplinskas told CBC News the government is not yet ready to provide details on how or when the consultation will take place.

The pandemic effect

While the pandemic may have brought more attention to the issue of high-interest loans, it’s not clear what effect it’s actually had on lenders and borrowers.

Julian and Ringuette said they’ve heard of people being forced to turn to such loans to get through a difficult year of job losses and reduced hours. The loans industry, meanwhile, has said it’s seen demand for its services decline during the pandemic.

Lenders argue that if they are unable to offer high-interest loans, things will only get tougher for poorer Canadians.

“It is important to have lenders provide credit to Canadians who are denied loans from a bank or credit union,” said the CCFA. “These loans are high-risk and expensive to provide. It is important for policy makers to fully understand the need for licensed legal credit options and the costs to provide that credit.”

‘Two-class system’

Julian agrees that high-interest lenders exist because there often is no other option available to people who don’t have solid credit scores or collateral.

“The reality is that what we’ve created in this country is a two-class system, where those that have some assets can access lending, either short-term or long-term, at a reasonable cost,” he said. “And then those who have the least assets to actually offer up are the ones that are being most gouged by a system that doesn’t protect them.”

In Australia — where there is evidence that the pandemic has driven many people, young people in particular, into debt — the government warns against such loans but has blown hot and cold on the idea of taking legislative action.

The U.K. recently considered setting tighter controls on interest rates, but backed off over concerns that it would shut down access to credit for poorer people and embolden criminal loan sharks.

Several U.S. states, on the other hand, have limited the amount lenders can charge for payday loans and many states have imposed a 36 per cent cap on interest for instalment loans. There is also a federal prohibition on lenders charging interest rates over 36 per cent to members of the U.S. military (some lenders were known to set up shop near military bases).

Canada’s CCFA said those restrictions have effectively killed the payday loan industry in some states and warns that the same could happen here, leaving many low-income households without an alternative source of credit.

Peter Julian said the government should ignore those arguments and — rather than launching a lengthy consultation — should simply incorporate his bill, C-274, into the budget.

“Mr. Trudeau has the opportunity. The bill is there.”

***

Article by Evan Dyer for CBC News